Strategic natural risk management at ecological tipping points

– Concept Paper –

1. Introduction: The turning point for natural risks

In 2026, the global economy faces a turning point in the assessment and management of nature-related risks. While regulatory reporting requirements under the Corporate Sustainability Reporting Directive (CSRD) and European Sustainability Reporting Standards (ESRS) have shaped corporate behavior in recent years, there is currently a clear shift away from a purely bureaucratic compliance orientation toward evidence-based analysis of risks that threaten the very existence of companies.

The traditional understanding of materiality is being expanded by the Sustainserv Nature Materiality Gap Analysis (NMGA)framework. In a world where planetary boundaries are operational realities, the ability to identify and manage location-specific ecological tipping points will determine the long-term economic viability of companies.

2. Theoretical foundation: Pareto instead of symbolism

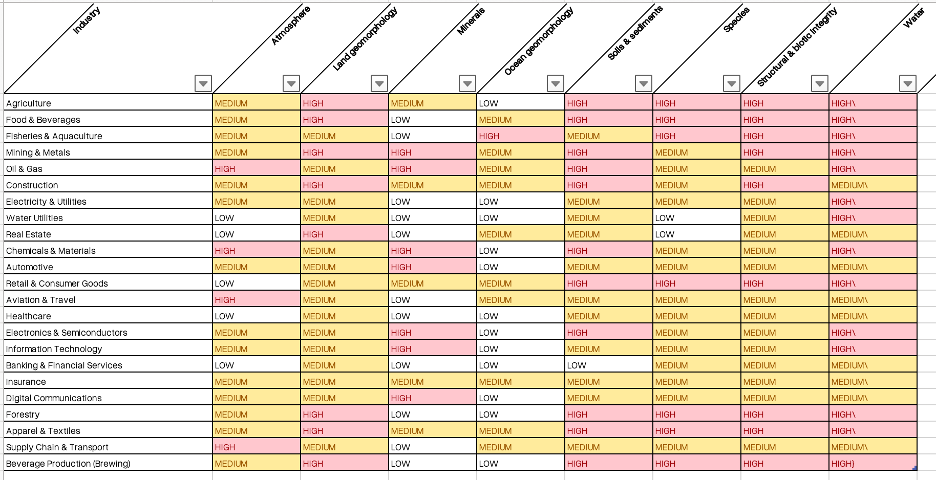

Not all industries are confronted with nature-related risks. In the operational approach to natural capital, there are a variety of approaches, ranging from selective measures such as setting up beehives on roofs to greening parking lots. These initiatives contribute to internal awareness and should not be discredited.

Nevertheless, a systemic view of ecological dependencies teaches us that we must keep an eye on cumulative effects, complex cascades, and the “long tail” of smaller environmental risks, but that the focus must necessarily be on economic materiality. The Pareto principle (80/20 rule) illustrates that a small percentage of sectors and locations are responsible for the majority of global nature-based risks. For effective management, it therefore makes sense to start strategically with those companies and value chains that are most dependent.

3. The limits of conventional materiality analysis

First, a limitations in common materiality analyses lies in their survey methodology. In a heuristic methodology, subjective assessments by stakeholders are usually translated into seemingly exact scores. While this approach may be appropriate for social issues, where topics are often only explored in a subjective, non-evidence-based manner, the methodology is not optimal for nature-related issues, where it is possible to collect scientific data. Additionally, in materiality analyses, social aspects such as work-life balance are often given equal and undifferentiated weight alongside ecological cluster risks, even though the former are characteristics of modern corporate management but have little potential to ruin companies.

On the other hand, it is usually nature-related aspects that are material because they can damage business models so severely that the viability of companies is affected. Especially when it comes to nature-related risks, well-known frameworks such as GRI or ESRS remain superficial. This is because data point specifications simply do not measure what they need to measure in order to make reliable statements about nature-related aspects. The example in Exhibit 1 illustrates our argument.

Exhibit 1: The pitfall of quantitative reporting

A specialty chemicals company based in the Bavarian Forest draws water from a nearby river for cooling purposes. The ESRS sustainability report correctly documents the withdrawal; since the water is returned in full without any loss, there appears to be no risk.

However, what is ignored is:

- Thermal pollution: The water is returned at a temperature 4°C higher, which causes massive damage to local biotopes.

- Dependency risk: Production has already had to be scaled back when water levels are low.

The fact that an auditing firm certifies this report without marking the economic risk of water scarcity as material underscores the “materiality gap.” Information on consumption and withdrawal says nothing about the proximity to the tipping point.

Exhibit 2: The pitfall of box-ticking on biodiversity

A European manufacturer of cancer treatments derived from marine resources reports several biodiversity-related impacts, risks, and opportunities in its ESRS sustainability statement, including biodiversity loss in the value chain, compliance risks, and the declining availability of marine invertebrates. Because these items appear in neat IRO tables and the report is audited by a Big Four firm, there seems to be no immediate threat to the business.

However, what is ignored is:

- Ecological tipping points: The company’s core assets depend on marine ecosystems that face symbiosis collapse from warming, ocean acidification, and pipeline-level biodiversity loss—changes the firm itself labels as irreversible over medium to long time horizons.

- Business-model dependency: There is no quantified assessment of how the loss of specific habitats and species, supply-chain restructuring, or new access rules for marine genetic resources could choke off future blockbuster candidates or drive steep cost increases.

- Regulatory shock risk: Despite looming CBD, Nagoya, High Seas, and other ocean-governance regimes, the company has neither performed a TNFD LEAP assessment nor analyzed scenarios for restricted access or new benefit-sharing obligations.

The fact that this disclosure passes audit without recognizing these nature-related tipping points as material again exposes the “materiality gap”. A list of biodiversity IROs says nothing about how close the company may be to losing its biological feedstock—and with it, its business model.

4. The concept of tipping points and leading indicators

In order to assess and manage the risk of dependence on nature-related materials, in the case of the specialty chemicals manufacturer water, the company must understand tipping points. Consciously or unknowingly ignoring tipping points leads to a form of strategic blindness that prevents companies from managing in a timely manner those factors that could ruin them in extreme cases.

The core of our approach is not to measure quantities, but to identify risks arising from proximity to ecological tipping points. A tipping point is the moment when a system loses its resilience. Time delays are critical here: a system may already have collapsed (overshoot and collapse) before the damage becomes visible in the balance sheet.

In a corporate context, this means that measuring lagging indicators (already documented damage) is strategically disastrous. Instead, leading indicators must be used to measure the rate of change and remaining resilience of a system. Our approach focuses on the financial and strategic integrity of materiality analysis and defines a risk as material if it impairs the organization’s ability to pursue its strategy or protect its enterprise value from the collapse of critical natural systems.

5. The economic reality of “impact”

Our focus on economic consequences does not stem from moral prejudice. Only by classifying environmental issues as critical risk drivers can they be given the necessary economic bite. Environmentally damaging behavior is material for three hard reasons:

- Capital costs & WACC: Banks and investors increasingly view the destruction of environmental resources as a systemic risk. “Nature sinners” risk being considered uninvestable or paying massive risk premiums on their financing.

- Physical inevitability: The destruction of one’s own production base (e.g., contamination of the process water used) is the purest form of economic materiality.

- Arbitrage limits: Relocating to countries with weak regulations (e.g., India) often leads to regions that are already much closer to ecological collapse. Fleeing the law leads directly into the arms of resource scarcity.

Consciously or unknowingly ignoring tipping points leads to a form of strategic blindness that prevents companies from managing the factors that could ruin them in extreme cases in a timely manner.

6. The NMGA assessment scheme: nine cascades

The practical application is carried out in a hierarchical logic of nine cascades:

Phase 1: Physical dependency audit

The goal is to determine whether the company is destroying its own production bases or is existentially dependent on dwindling natural assets.

- 1.1 Resource self-sufficiency & feedback loops: This examines whether the company is endangering the very resources on which it depends through emissions or extractions (e.g., process water pollution).

- 1.2 GVA criticality and threshold analysis. This determines whether the dependence of gross value added (GVA) on a dwindling natural component exceeds the critical threshold of 70%.

- 1.3 Operational resilience & substitutability. Assessment of the substitutability of ecosystem services and examination of whether local degradation (e.g., forest loss > 30%) endangers the physical integrity of the facilities.

Phase 2: Social license & market audit

Assessment of the risk of losing market share or being excluded from markets due to public exposure or lack of ecological integrity.

- 2.1 Transparency exposure. Measurement of the risk that practices will be documented by satellite monitoring or real-time sensor technology.

- 2.2 Marketability & supply chain resonance. Examination of the risk of exclusion from the supply chains of global players or from green building tenders.

- 2.3 Strategic market positioning (brand stress test).Stress test of brand value to determine the share of sales that would be lost if ecological credibility were lost.

Phase 3: Economic financial market audit

Ensuring investability and avoiding impairments.

- 3.1 Systemic long-tail risks & liability. Identification of long-term liability claims that could make the company “uninvestable” for banks.

- 3.2 Strategic resilience (reverse stress test). Determination of the points at which resource shortages or price increases lead to the collapse of EBITDA.

- 3.3 Materiality gap & valuation (WACC & terminal value adjustment). Adjustment of valuation parameters (increase in WACC, setting terminal value to zero) when ecological collapse points are reached.

7. Linking tipping points with financial indicators

The final part forms the mathematical bridge to company valuation. It specifies how identified “kill factors” are translated into hard financial indicators such as WACC, terminal value, or EBITDA at risk using lead indicators. For details, please see our paper Nature-Adjusted Economic Value (NAEV).

Financial mathematical validation and DCF integration

Ecological tipping points are linked to financial indicators through an economic threshold analysis that translates physical natural capital assets via their ecosystem services (dividends) into business risks.

The principle of reverse stress testing

Instead of starting with complex biological models, this approach begins at the company’s financial collapse point. Management first identifies the point at which the business model collapses – for example, due to a 30% loss in EBITDA – as a result of the loss of a critical resource or extreme price increases. Only then is the ecological probability of the resource used reaching its specific tipping point examined.

Metric mapping: From natural assets to financial metrics

The framework correlates the eight ENCORE natural capital components (ENCORE, 2026) with forward-looking lead indicators and the resulting impact on financial metrics.

| Natural asset (ENCORE) | Ecosystem service | Lead Indicator (Early Warning) | Financial metric (impact) |

| Water | Water supply | Aquifer depletion rate (GRACE) | OpEx: Replacement water/downtime costs. |

| Soil | Maintaining fertility | Humus trend (SOC < 2%) | Yield: decline / impairment. |

| Species | Pollination | Pollinator abundance per hectare | Revenue: Loss of revenue per cycle. |

| Land geomorphology | Protection from hazards | Annual forest loss rate (> 30%) | CapEx: Infrastructure repair costs. |

| Ocean geomorphology | Coastal protection | Coral bleaching index (> 50%) | EBITDA: Collapse of tourism/fishing revenues. |

| Minerals | Material supply | Ore grade trend per mine | Investment: Higher costs / stranded assets. |

| Atmosphere | Air pollution control | Trend in PM2.5 emissions | Liability: Long-tail risks / health. |

| Ecosystem integrity | Systemic resilience | Habitat fragmentation (EII < 0.4) | WACC / Terminal value. |

GVA at risk and terminal value

A risk is considered existential if more than 70% of gross value added (GVA) depends on a resource that is approaching a tipping point. In discounted cash flow (DCF) valuation, this leads to a massive increase in the risk premium (WACC), as investors pay greater attention to systemic stability. If a system approaches collapse, the terminal value (residual value) falls toward zero, as the physical assets become economically worthless without their ecological basis.

8. The second Pareto iteration: Identification of the “kill factors”

Representation as a risk cascade: An effective representation is provided by a Pareto diagram of natural risks. On the X-axis, ecosystem services are sorted according to their financial impact. The Y-axis shows the potential financial damage. A cumulative curve (the “Pareto curve”) impressively visualizes how the first 2-3 services already reach the critical threshold of existential threat.

Background: There are over 20 different ecosystem services (according to the CICES classification), from pollination to water regulation. In practice, it has been shown that for a specific business model (e.g., beverage manufacturer), only 20% of these services (e.g., surface water availability and water purification) are responsible for 80% of operational continuity. From a forward-looking risk management perspective, companies do not need to protect every detail of nature, but primarily the services that form the “backbone” of their value creation.

Geographical hotspots of dependency: Dependencies are location-specific. Often, 80% of critical inputs come from only 20% of the sourcing areas or locations. Take semiconductors, for example: production is extremely dependent on water. A single catchment area (hotspot), which accounts for only a small part of the global area, can represent 80% of a corporation’s production risk.

Financial materiality

The TNFD(Taskforce on Nature-related Financial Disclosures) uses the Pareto principle to identify “priority locations.”

- Screening: Identification of all points of contact with nature.

- Pareto filter: Selection of the 20% of locations/processes that bear 80% of the financial risk from nature loss (e.g., due to the loss of pollination in agriculture).

| Ecosystem service (BEES) | Share of financial risk (GVA at risk) | Cumulative risk | Strategic classification |

| Freshwater supply | 50 | 50 | Kill factor (priority 1) |

| Pollination | 30 | 80 | Kill factor (priority 2) |

| Erosion control | 10 | 90 | Strategic management |

| Soil fertility | 5 | 95 | Monitoring |

| Other 15+ services | 5 | 100 | Long tail / “Nice-to-have” |

Exemplary risk concentration (example: agriculture/food):

Focus metric: GVA at Risk (Gross Value Added at Risk) is often used for this purpose. The illustration makes it clear: if these 20% of natural assets are not managed, protecting the remaining 80% is almost economically irrelevant.

9. Paradigm shift in risk management

The concept of non-linear risk management is gaining importance as traditional linear models reach their limits when it comes to systemic crises and ecological tipping points. While classic risk analyses often assess risks in isolation according to probability and damage level (heat map), the non-linear approach recognizes that systems have thresholds. Small causes may have little effect below a threshold, but once the threshold is exceeded, they can lead to sudden collapse.

Connections in the COSO 2017 update

The COSO ERM Framework (COSO: The Committee of Sponsoring Organizations of the Treadway Commission, 2017) has anchored this philosophy in its 2017 update.

- Complexity of risks: COSO emphasizes the interconnectedness of risks and warns against viewing them in silos, as interactions lead to nonlinear outcomes.

- Adaptive capacity and resilience: Focus on the organization’s response to unexpected, sudden changes. Use of scenario analysis to simulate extreme scenarios.

- Integration into strategy: The greatest risk often lies in the strategy no longer being appropriate for the environment. The strategy itself becomes a risk object.

| Feature | Classic risk matrix | Tipping point matrix (non-linear) |

| Focus | Static snapshots of individual risks. | Dynamic thresholds and paths. |

| Mathematics | Probability X% Amount of damage | Simulation of cascade effects. |

| Management | Mitigation: Limit/insure damage. | Resilience & transformation of the system. |

| Materiality | What does the risk cost us? | Could it destroy our livelihood? |

Comparison: Classic vs. tipping point matrix

In this context, the integrity of a business model means protection against non-linear risks. A company with high integrity recognizes social or environmental tipping points before they occur because it has “ethical sensors” and does not rely solely on legal compliance.

10. Global context and outlook

The year 2026 marks the transition from sustainability ambitions and reporting to financial reality and measurable business value.

Convergence of standards: TNFD and ISSB

The International Sustainability Standards Board (ISSB) has decided to enter the standard-setting process for nature-related risks, using the framework of the Taskforce on Nature-related Financial Disclosures (TNFD) as a basis. In April 2026 the ISSB decided that its work on nature-related reporting will proceed through a non‑mandatory IFRS Practice Statement on nature-related disclosures, rather than a new mandatory nature standard. The TNFD will complete its technical work by the third quarter of 2026 and then focus on supporting the ISSB’s work program.

Progress at SBTN (Science Based Targets Network)

The SBTN is working to enable companies to set science-based targets for nature besides climate. By mid-2026, the SBTN will publish its second and final major technical guidance, which will expand coverage across land, freshwater, and oceans. The first companies (e.g., GSK, Holcim, Kering) have already published validated targets for freshwater use and land use. The SBTN is recognized as a critical corporate target-setting mechanism for nature transition plans.

Trends in nature risk management 2026

- Execution over ambition: Companies face the harsh reality of costs, infrastructure, and geopolitical risks. Sustainability becomes an “engine of competitiveness” and design logic.

- Data revolution: The TNFD recommendations for enhancing the Nature Data Value Chain aim to improve the discoverability and quality of nature data as a global public good. The planned Nature Data Public Facility (NDPF) is intended to give SMEs access to risk assessments.

- Climate risk as a live financial issue: Physical hazards are evident in core markets (wildfires, water stress), making adaptation a top priority on the strategic agenda. Nature-based solutions such as forest restoration and water management are becoming essential to securing access to resources.

- Re-pricing of sectors: New regulatory tightening or product bans can revalue sectors faster than governance cycles can respond. In 2026, the benchmark will shift from comprehensive description to the credible embedding of scenario analyses in capital allocation decisions.

Get in touch. We are happy to tell you more about it.