Summary

Sustainserv Zurich, and the auditing and tax consulting firm Dr. Kleeberg & Partner GmbH, Munich, jointly examined the sustainability reporting practices of selected medium-sized and family-owned companies in Bavaria. In each case, they used the most recent reports issued, which were published on April 1, 2020 or June 1, 2021. In terms of the disclosure deadlines applicable to medium-sized companies, these typically concerned the reporting years 2018 or 2019.

The aim of this study was to determine whether issues relating to sustainability and climate change are already a mainstay of the corporate strategy at these companies – which are not (yet) legally required to report on sustainability – and thus also appear in their reports. It was found that, although the companies are essentially aware of society’s growing interest in sustainability issues – both generally and with regard to their products –, they have not yet addressed the topic consistently and uniformly in their corporate communications. To date, medium-sized companies have largely neglected the opportunity to grant stakeholders insights into their economic, ecological, and social policies by means of sustainability reporting.

Given changing attitudes in society, various sustainability “megatrends,” and increasing regulatory requirements, sustainability reporting at medium-sized companies is due to become a far more significant issue in the coming years. These companies, in particular, need to be mindful of the fact that a full and frank engagement with the issues involved in clear, proactive sustain-ability reporting will allow them to grasp the opportunity not only to meet the growing requirements and demands of stakeholders but also to stand out from the competition.

Download the full article here:

Background and (legal) requirements for Sustainability Communications

Sustainability is high on the agenda of many companies today, and includes climate protection – in operations and in the supply chain, in products, and in services. Europe’s aim to achieve climate neutrality is a mammoth task. The EU has chosen to adopt a European Green Deal, backing it up with an ambitious action plan (the EU Action Plan on Financing Sustainable Growth). This shows how two goals are closely interlinked – environmental protection and the promotion of robust economic growth. Europe wants the private sector to contribute to making the continent climate-neutral, from which it, too, will benefit.

From today’s perspective, the requirements of the European Non-Financial Reporting Directive (NFRD; EU CSR Directive (2014/95/EU)), known in Germany as the CSR Directive Implementation Act (CSR-RUG), were essentially a prelude to these plans. The reporting requirement makes certain sustainability data on many larger companies available by regulation. And this policy train continues to gather momentum. Following extensive deliberations by European policymakers on an NFRD amendment, the draft for new EU regulations on sustainability reporting has been available since April 2021. The draft Corporate Sustainability Reporting Directive (CSRD) is intended to largely replace the current regulations on non-financial reporting as set out in the previous EU CSR Directive and the CSR-RUG in Germany.

In Germany, Section 289b(1) of the Commercial Code (HGB) currently requires, in particular, large corporations (Section 267(3)(1) HGB) that are capital market-oriented (Section 264d HGB) and employ an annual average of at least 500 people to supplement their management reports with a non-financial statement. The same applies to the companies defined in Section 264a HGB, provided they meet the requirements. The reporting requirement also applies to banks and insurance companies, for example. Non-financial statements should contain company information relating to environmental, social, and employee concerns, to respect for human rights, and to combating corruption and bribery.

In addition to new reporting content, the draft of the new European sustainability directive provides, in particular, for a significant expansion in the number of firms required to make disclosures, which will naturally also have an impact on German companies: In future, all companies listed on a regulated EU market will be affected, regardless of their size – the only exception being micro-enterprises.

Also falling under the new requirements are non-capital market-oriented companies that exceed at least two of the following three size criteria (large corporations): 20 million euros in total assets, 40 million euros in revenue, and an average number of 250 employees.

According to estimates, this would mean that, in the future, around 15,000 companies in Germany would be required to incorporate sustainability issues in their management reports, compared to the current 500.1 The expanded reporting requirement is due to apply to large corporations (irrespective of their capital market orientation) as early as 2023. For capital market-oriented small and medium-sized companies, the rules are set to apply later, from 2026 on.

This thus confirms the expectations expressed by many in the past that medium-sized companies will be subject to reporting requirements in the medium term. Even though the EU Directive is still at the draft stage, and its content, if adopted, will need to be transformed into German law, there is already much to suggest that regulations will indeed be tightened.

In addition, the EU Commission wants to place the “new” sustainability report on an equal footing with the financial reporting in terms of auditing. In addition to an audit by a company’s supervisory body (e.g., the supervisory board or audit committee), auditors will in future be expected to carry out not only a formal but also a substantive audit, i.e., of the content. This planned change again shows the importance that sustainability reporting will have in the future.

In view of the growing interest in and, especially, awareness of sustainability among intended readers, all companies would be well advised to engage early on and in detail with the requirements relating to appropriate sustainability communications. Excessive hesitancy could end up being “punished” by the market just as much as a purely superficial engagement with the relevant issues.

In order to understand how prepared medium-sized companies are to respond to this pressure in a timely manner, the management consulting firm Sustainserv GmbH and the auditing and tax consulting firm Dr. Kleeberg & Partner GmbH jointly examined reporting practices at selected medium-sized and family-owned companies in Bavaria to determine their relative strengths and weaknesses. The analysis focused on sustainability and, in particular, climate issues. In addition to reporting in the (group) management report, voluntary sustainability communications – e.g., in separate reports or on company websites – were also assessed. 1 See DRSC, CSR study, January 2021, paragraph 257

Sustainability reporting is set to become mandatory for some 15,000 companies in Germany. The first extended reporting requirements are due to apply from 2023 on.

Description of the study and methodology

The study centers on the following question: What is the current situation at non-listed companies, i.e., those not yet officially subject to reporting requirements? To investigate this question, we analyzed a representative sample of around 50 of the largest medium-sized and family businesses from a range of sectors in Bavaria. We looked at both the (consolidated) financial statements and management reports for the 2018 and 2019 reporting years (mandatory reporting), and the sustainability websites and reports (voluntary reporting) issued by these firms. The following points were of particular interest:

Reporting / transparency

- Do these companies disclose their non-financial KPIs?

- Is there a sustainability website or report?

- Are KPIs and targets related to climate change disclosed?

- Which frameworks do the companies employ?

Strategy

- Do the companies see climate change as a risk and/or an opportunity?

- Do they specify climate-friendly or sustainable products?

- Is their strategic focus consistent across mandatory and voluntary reporting?

Comparison of 2018 and 2019 reporting years

- Does the analysis reveal significant changes?

Extended sustainability reporting in the future is to be audited not only formally, but also in terms of its content.

Results of the study

Reporting on sustainability and, in particular, climate issues by various medium-sized companies in Bavaria shows that many have already taken their first, promising steps. There still remains much to be done, however – in terms of both the robustness of the fundamentals and consistency. Beyond this, the analysis noted only minor progress in the disclosures for the 2018 and 2019 reporting years.

Of note is that a clear majority of the companies surveyed have put in place environmental and energy management systems, and over a third of them mention climate change as a risk or opportunity, at least indirectly, in their mandatory reporting. Be that as it may, only a minority set out quantitative KPIs that demonstrate the issue’s strategic significance to the company. In addition, the same issue is often documented and strategically assessed differently in the management report and in the voluntary sections of the report. This makes it difficult for addressees of the corporate communications to form a clear picture of how seriously sustainability – and consequently sustainability performance and outlook – is considered within any one company.

Sustainability communications common, especially with regard to products

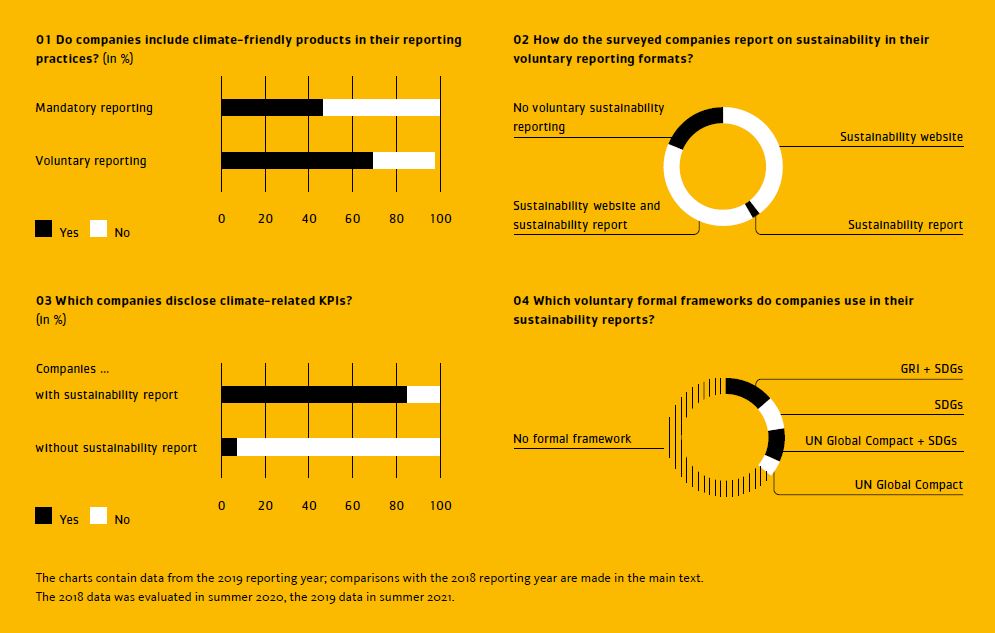

The majority of the surveyed companies’ mandatory reporting – i.e., in the (consolidated) financial statements and management reports – makes clear that sustainability issues feed into their corporate strategies. Within this reporting, too, almost half of the company’s report on their sustainable or climate-friendly products and services. This approach makes it possible to place a company’s sustainability impacts in a good, “green” light, clearly highlighting the benefits to customers and the company itself, and increased marginally between 2018 and 2019. (chart 01)

It is therefore not surprising that offerings relating to sustainable and climate-friendly solutions are also among the topics that the companies surveyed like to address in additional, voluntarily published formats for sustainability communications. For around two-thirds of the companies, these voluntary formats are a sustainability section on their websites or a dedicated sustainability website. More than one-third of the companies even publish a separate sustainability report. Overall, it is seen that the scope and detail of information on sustainability in these voluntary formats goes beyond what is disclosed in mandatory reporting. This is not only the case with regard to products and services, but often concerns the company’s entire, overarching approach to sustainability. Compared to the prior year, there was a 6% increase in the number of companies surveyed that published a sustainability report in the 2019 survey year. (chart 02)

Targets and KPIs almost only provided in voluntary communications

Pursuant to Section 289(3) HGB, Section 315(3) HGB, and GAS 20 “Group Management Report,” large companies must include relevant non-financial KPIs in their (group) management reports or, if they are published elsewhere, must refer to these publications. This is now the case for a large proportion of the companies surveyed. However, in many cases, companies communicate little about climate and energy issues in their mandatory reporting. Quantitative details such as KPIs and targets are few and far between. (chart 03)

Voluntary communication goes further on this issue, with most companies that publish a sustainability report providing at least certain KPIs and targets on topics such as energy consumption, renewable energy, and greenhouse gas emissions. This gives their readers the opportunity to form an independent opinion of their companies.

Few reports based on established systems

Only companies that publish a significant amount of voluntary reporting on sustainability relate it to established systems. None of the analyzed (group) management reports, for example, refer to the Sustainable Development Goals (SDGs) of the United Nations, although some are starting to use them in their sustainability reports. The sustainability reporting frameworks of the GRI (formerly Global Reporting Initiative) and the UN Global Compact are, however, used by about one-third of the companies that publish a dedicated sustainability report. (chart 04)

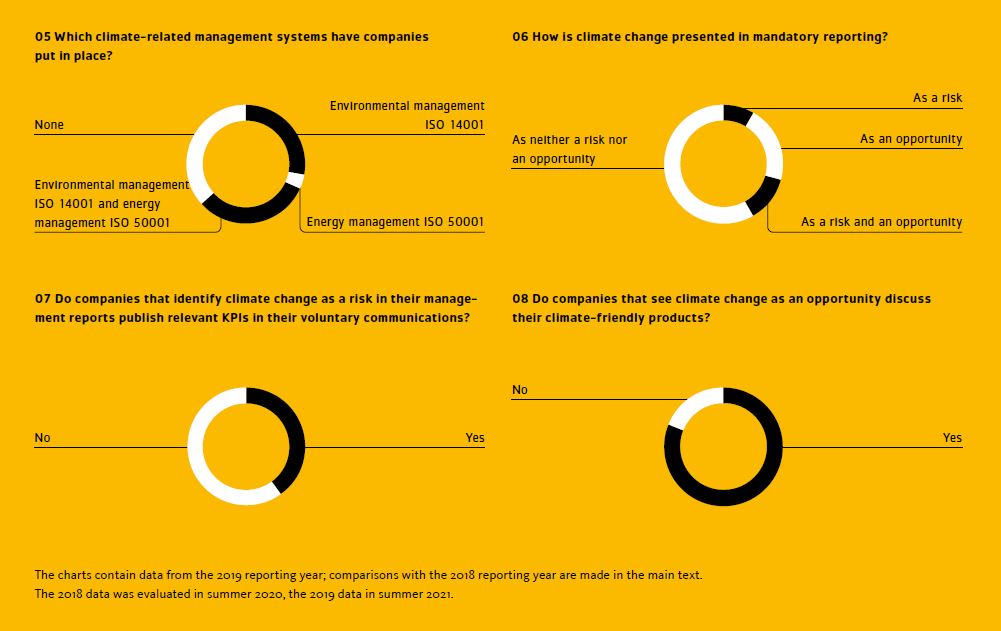

By contrast, the surveyed companies do rather well on the “Management systems for sustainability” point. More than half are certified according to the ISO 14001 environmental management system. In addition, around a third operate an energy management system certified to ISO 50001. There are, then, clearly elements in place to develop an effective sustainability and environmental strategy. To date, however, they have not been used often for a systematic disclosure of sustainability practices. (chart 05)

Risks and opportunities not uniformly assessed in the reports

Within mandatory individual or group reporting, well-founded information on climate change is most likely to be found in the risk and opportunity report, where readers can find out whether climate change is a risk and/or an opportunity for the company concerned. The surveyed companies mostly refer to changing market conditions in areas such as electromobility, renewable energy, or energy costs. Product developments with which the companies intend to profit from trends are also mentioned, but clear quantitative climate protection targets and KPIs are only disclosed in exceptional cases. (chart 06)

This point also reveals the greatest discrepancy between mandatory and voluntary reporting. Voluntary reporting rarely states whether climate change represents a risk or an opportunity for the company. In this context, climate protection tends to be presented as a facet of corporate responsibility. As an example, companies will set out how they intend to help reduce greenhouse gases or achieve carbon neutrality in the future.

Moreover, where climate change is identified as a risk or opportunity, voluntary and mandatory reporting are strikingly inconsistent. Only around half of the companies that present climate change as a risk in their (group) management reports discuss it in detail in their voluntary communications, citing relevant KPIs and targets. Similarly, only a minority of companies that voluntarily present climate-friendly or sustainable products describe climate change as an opportunity in their (group) management reports. (charts 07 and 08)

Conclusion

The study revealed that the companies surveyed are fundamentally aware of the problems of climate change, their associated responsibility, and the growing interest of their customers and other stakeholders in sustainability-related information. This is particularly evident from the fact that the vast majority of the companies report, at least on a voluntary basis, on their range of sustainable and climate-friendly products, as well as their handling of natural resources and associated solutions. A minority also already publish specific KPIs in various voluntarily published formats, for example on operational energy consumption and greenhouse gas emissions, and quantify the company’s goals with regard to a more conscious reckoning with nature and its resources. Compared to voluntary communications, mandatory reporting has so far been treated rather like a poor relation when it comes to sustainability-relevant information. It is becoming clear that many companies are not yet using the topic strategically and consistently to manage relevant risks and exploit potential opportunities.

Given the impending tightening of legal requirements arising from the current draft of the EU’s Corporate Sustainability Reporting Directive (CSRD), medium-sized companies can only be advised to take advantage of the grace period resulting from the proposed EU directive. In particular, this applies to companies that have not yet dealt (in detail) with the topic of sustainability reporting. Here, it is important to bear in mind that sustainability reporting should be seen as an opportunity and as an important instrument of corporate communications. A clear sustainability strategy can act to secure a company a strategically advantageous position in the market and make a key contribution to its attractiveness in the eyes of customers, potential employees, and other business partners.

In an age of carbon-neutrality targets, political requirements, and rapidly changing awareness of the environment, climate, and sustainability, coherent and consistent reporting on the subject of sustainability is becoming increasingly important. In this context, companies need to embrace communications that are consistent throughout the business and are not contradicted by the financial reporting. It is no longer sufficient to report on sustainable products or general sustainability solutions. The capital market is also increasingly differentiating on the basis of how companies deal with the issue of sustainability. In other words, “greenwashing” will no longer do. What we need is a culture of sustainability promoted and embraced throughout a company, which must be reported on – not least for reasons of self-interest. The legislature has formulated clear ideas and will not hesitate to successively tighten reporting requirements. Alongside the capital market, it is especially medium-sized companies that must now report on the “good” things they do. In the end, after all, only long-term sustainable action can be successful.

Sustainability reporting should be seen as an opportunity for corporate communications to contribute to the attractiveness of the company in the eyes of customers, employees, and business partners.

Findings from the study conducted by Sustainserv GmbH and Dr. Kleeberg & Partner GmbH, as seen in the latest issue of The Reporting Times published by the Center for Corporate Reporting (CCR).

Get in touch. We are happy to tell you more about it.