The European Commission adopted an Action Plan on Sustainable Finance in March 2018. In December 2019, Commission President Ursula von der Leyen presented the “European Green Deal,” which aims to reduce net emissions of greenhouse gases in the European Union to zero by 2050. This would make Europe the first climate-neutral continent.

These two initiatives are the cornerstones of any EU activity in the field of sustainable financial markets. The EU has thus set itself far-reaching sustainability goals. In fact, many consider the “European Green Deal” to be as ambitious as the reconstruction after the Second World War.

The EU’s aim is to commit the financial sector to act as a catalyst for the transformation of the real economy. This objective will significantly change the interfaces and cooperation between financial institutions and companies in all sectors. As new information comes into play that influences decisions (for example, investment or credit decisions in the capital market and strategic decisions in companies), communication between both groups of actors will also change.

In addition to investors and financial analysts, corporate communications, investor relations, and corporate development can also benefit from strategically positioning themselves in relation to these developments. This article shows how.

Companies will feel the pressure on their financial market partners

With regard to environmental, social, and governance (ESG) issues, in the past only a minority of investors have had contact with the companies in their investment portfolios. In the future however, ESG issues will become a necessary part of the standard interaction between the financial sector and the real economy as regulatory pressure on the financial industry increases within the European Union. Sustainability in the financial sector will be incorporated into numerous regulatory frameworks, creating direct pressure on EU-based financial service providers and, as a result, on European companies in all sectors. To a certain extent, regulatory and market requirements will also affect financial institutions and companies based outside of the EU if they offer financial products in the EU or have economic relations with European financial service providers.

Unlike previous regulatory measures, the aim of the regulations will be to work toward an economically efficient and sustainable global financial system that provides more capital for sustainable investment. The regulator thus uses the capital market to influence the real economy.

Problem areas from the perspective of the EU

The EU has defined three problem areas regarding sustainable investment and has adopted overarching measures to address them. With the guiding principle of voluntary to mandatory, the aim is to curb the proliferation of non-standardized sustainability approaches and disclosures of past decades and transfer this field into a regulated market. This will require addressing the following issues:

- Too little consideration of ESG. In the EU’s view, banks, asset managers, and institutional investors do not take ESG risks sufficiently into account in their investment and lending decisions, as they have too little knowledge of sustainability and often underestimate the resulting risks. In the future, institutional investors should be obliged to take sustainability risks into account in asset allocation. In addition, the EU is investigating whether ESG risks should be reflected in capital adequacy.

- No clear definition of sustainability. Responsible Investing, Ethical Investing, or ESG? According to the European Commission, the large number of terms alone shows that a standardization of terminology is necessary to prevent “greenwashing” and “camouflage.” The EU has therefore decided to introduce a so-called taxonomy, which will be the basis for clear standards and labels that provide investors with certainty that sustainable financial products are genuinely sustainable.

- Too little information about corporate sustainability in the market. The EU believes that there is too little information on sustainable business practices circulating in the market, much of which is not qualitatively valuable. This applies both to the integration of ESG risks throughout the financial industry and to financial products explicitly offered as sustainable. The EU measure aims to improve the disclosure of non-financial information. According to the EU Action Plan, investors need detailed information on how much turnover a company generates from sustainable and non-sustainable activities, for example, to be able to determine the weighting of shares in a portfolio. Among other things, this will mean that companies will have to publish significantly more and also different data on the concrete basis of their value creation.

“I believe that sustainable investing will become the new “normal.” To do this, we need to know, among other things, the extent to which the purpose of a company is sutainable – or, to be more specific: what proportion of its turnover is generated from sustainable business areas.

This is exactly where the EU taxonomy will set a standard. We expect from companies that they disclose corresponding information.”

Dr. Henrik Pontzen, Head of ESG in portfolio management at Union Investment

High demands are placed on investors to take ESG into account

In the future, investment advisors will be required to offer sustainable investments to their clients, such as private investors or smaller institutional clients (Action Plan point #4). They must therefore ensure that the customers are sufficiently informed about sustainable investments. This will also affect larger institutional investors and asset managers who will in addition have to disclose their investment strategies and effective investments—their “ESG footprint” (Action Plan point #7). The increasing use of ESG data by investment advisors, institutional investors, and asset managers will lead supporting companies such as data service providers and sustainability rating agencies to apply even more ESG criteria and demand corresponding data (Action Plan point #6). While many ESG data and rating providers already make extensive use of ESG information, the EU seems to be expecting a single rating system with data points that use standardized protocols, independent of the rating service provider. In our perception, if necessary, the EU would likely be ready to “help” with regulation to achieve this.

What does this mean for communication between the capital market and companies?

Companies must prepare for far-reaching changes, including:

- Provide more material ESG data. There are signs that companies will have to report more and different ESG data in the future and provide investors with information on the materiality of this data. However, this alone is not enough:

- Explain how non-financial aspects influence business results and enterprise value. The integration of financial and CSR reports will experience a renaissance as companies are expected to relate their ESG data to economic or financial metrics. Companies can take advantage of this by developing, for example, ratios and narratives in which the sets of information validate each other’s plausibility. In our view, while aligning with the guidelines of the International Integrated Reporting Council (IIRC) makes sense, it is by no means the only way of implementation.

- Make sure senior management is fluent in ESG matters. In dialogue with capital markets (for example, in investor meetings or annual general meetings), senior management must be able to speak to and explain ESG issues, as these topics are becoming increasingly important.

Senior management is obliged to manage the company in a sustainable manner

The EU will also expect senior management of companies to implement sustainable management practices. Even though the catalogue of measures in the EU Action Plan is mainly aimed at the financial sector, the call for the promotion of sustainable corporate management (Action Plan point #10) clearly also concerns other kinds of companies. This demand may sound like a soft ask that could be fulfilled by simple declamation. However, this impression is deceptive.

The EU expects sustainability to be integrated into corporate risk management. This is anything but trivial. Technically adequate risk management requires pricing in the extent and probability of damage and should be designed in such a way that environmental, social, and governance risks can also be recorded, managed, and reported as precisely as possible, in line with accounting principles (clear, comprehensible, complete). Beyond risk management, companies should also anchor and strengthen sustainability strategically, such as by designated functions, so that it is well embedded in organizational and functional terms.

“I am convinced that companies with a strong ESG offering can create long-term value. Proactive thinking and action in the area of ESG has become even more urgent recently.

Society’s expectations of companies have changed, and the size and impact of a company go hand in hand with its increased responsibility for commitment and transparency.”

Oliver Maier, Head of Investor Relations, Bayer AG, and President of the German Investor Relations Association (DIRK)

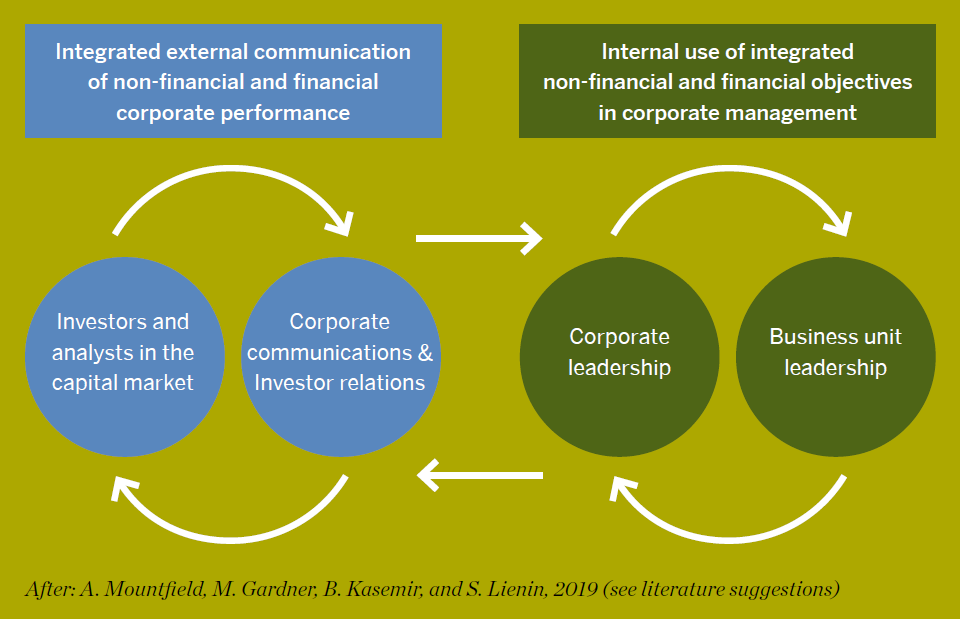

Consistent communication, consistent leadership

The EU Action Plan with its interlocking packages of measures affects almost all market participants including financial institutions and companies in all sectors. The implementation of the EU Action Plan will involve a significant effort for all of them. As with any investment, the question arises of how to generate as much added value as possible. Ideally, non-financial, or more precisely, pre-financial data, which will have to be provided and used in the future for capital markets or risk management, will generate double added value. For example:

- As good “compliance” strengthens the institutional reach, meeting the data requirements of investors and intermediaries will be in the companies’ interest. External communication between the financial market and companies will be significantly strengthened by information on long-term value creation potential by the company.

- Advantages for internal management, such as internal communication between corporate headquarters and business units, will also be apparent. Strategically well-chosen ESG data can be very valuable for internal management, which is made more effective by such non-financial management indicators.

Reliable, end-to-end integration of non-financial and financial information creates consistency between what the company communicates to the capital market and what it actually does within the group and its business units.

How do you position yourself successfully?

The EU Sustainable Finance Action Plan sets clear and far-reaching requirements for financial institutions: they will need to change in order to adapt. For companies in other sectors than financial services, however, there are considerable “pull effects” from the higher information needs of the financial market. Here, many companies are still faced with the question of what this will mean for them and how they can react to it.

We offer the following recommendations for corporate communications, investor relations, and senior management on how companies can position themselves in relation to the EU Action Plan and the resulting requirements for non-financial transparency in a manner that will provide them with clear added value:

Recommended Actions

- Create an integrated narrative. Eliminate the separation of financial and non-financial topics and data in external communications and internal management. There is no such thing as a financial reality separated from a sustainability reality concerning a company. It’s one business with one story that needs to be presented in a single narrative to bring investors, customers, and employees on board.

- Bring internal functions together and bundle strengths. Strengthen the cooperation between Corporate Communications, Investor Relations, Accounting, and Corporate Sustainability to sift through and integrate financial and non-financial data and focus on the essentials.

- Develop an “Integrated Set of Facts.” Your internal communication and external reporting should include a recurring, compact set of reporting items in which non-financial or ESG data explain and contextualize economic or financial facts. This makes the long-term value drivers for the company understandable and tangible.

- Ensure consistent, strategic communication. Get an overview of the non-financial key figures that you already disclose in various report formats, and ensure consistency. Investors and other target groups are unsettled if, for example, a non-financial topic is presented as critical in the sustainability report but does not appear at all in the risk and opportunity report.

- Stay rigorously to the point. Focus this integrated approach on a few management-relevant topics and key figures and implement it rigorously in all reporting formats that are relevant to the capital market, the sales market, and the labor market.

The original text entitled “The EU Action Plan on Sustainable Finance – Opportunities for Corporate Communications, Investor Relations and Senior Management” by Ralf Frank and Dr. Bernd Kasemir was published as a supplement to the German edition of issue 16 of The Reporting Times, the trade journal of the Center for Corporate Reporting (CCR).

Literature suggestions:

Regulatory texts:

German Federal Financial Supervisory Authority BaFin (2019). Guidance notice on dealing with sustainability risks.

European Securities and Markets Authority ESMA (2018). Consultation Paper: On integrating sustainability risks and factors in MiFID II.

European Commission (2018). EU Action Plan for Financing Sustainable Growth.

European Commission (2018). Final Report 2018 by the High-Level Expert Group on Sustainable Finance.

How investors use integrated reports:

Arnold, M., Bassen, A., & Frank, R. (2018). Timing effects of corporate social responsibility disclosure: an experimental study with investment professionals. Journal of sustainable finance & investment, 8(1), 45-71.

On consistent communication and leadership:

Mountfield, A., Gardner, M., Kasemir, B., and Lienin, S. (2019), Integrated management for capital markets and strategy: The challenges of ‘value’ vs. ‘values’ sustainability investment, Smart Beta and their consequences for corporate leadership, in Rethinking Strategic Management, (ed.) Thomas Wunder, Springer, 105-128.

About “parsimonious” reporting:

Cohen, J. R., Holder-Webb, L., & Zamora, V. L. (2015). Nonfinancial information preferences of professional investors. Behavioral research in accounting, 27(2), 127-153.

Project Delphi (2016). The Material ESG Factors and Metrics that Drive Value.

Get in touch. We are happy to tell you more about it.