Every company confronts economic, social, environmental and governance issues that are relevant to sustainable business management. A systematic materiality assessment helps determine which topics should be considered in business or sustainability strategy development, in performance measurement and in reporting. A clear focus enables impactful sustainability management.

What are the advantages of a materiality analysis?

A well-structured materiality analysis is the starting point for coherent sustainability management. It clarifies the strategic focus, helps define suitable goals and KPIs, and sets the framework for internal and external communication.

In a materiality assessment, potentially relevant topics are evaluated from different perspectives to gain a comprehensive picture of the expectations of your business and its impact on society and the environment. Certain topics must be deliberately left out in order to focus on the most relevant areas. This allows you to ensure long-term business success, meet stakeholder expectations and contribute to sustainable development. Through the exchange with your stakeholders, you not only gather insight into their needs and expectations vis-à-vis your company but also strengthen your relationships.

How do we proceed?

At Sustainserv, we typically structure a materiality assessment in five steps:

1. Clarify the purpose

There are numerous ways to perform a materiality assessment. Between brief workshops and large-scale surveys of hundreds of stakeholders, there is a wealth of possibilities. The purpose of the assessment and the resources available provide the cornerstones of this process.

At the beginning, we clarify with you the purpose of the materiality assessment: Are we defining the thematic focus for a sustainability report? Are we focusing on the exchange with various stakeholders? Or are we (further) developing a sustainability strategy with comprehensive sustainability management? We also discuss which stakeholders you would like to involve in the process and how the results should be visualized.

2. Compile topics

Based on these answers, we select potentially relevant topics by considering standards such as the Global Reporting Initiative (GRI), SASB and the Sustainable Development Goals (SDGs); evaluating your industry’s most important topics; and weighing your company’s internal priorities. We then group the collected topics to obtain a number that can be reasonably assessed by your stakeholders.

3. Assess topics

The chosen topics are typically assessed by management representatives and stakeholders, including customers, employees, suppliers, NGOs, and external experts. This incorporates different perspectives into the assessment, resulting in a holistic picture of priorities, expectations and needs. Various formats can be used for the assessment including surveys, interviews, workshops and panels.

4. Visualize topics

After assessing the issues, we usually present the results in a materiality matrix, which shows a visual representation of which topics should be prioritized.

5. Validate topics

Finally, the results are presented to the company management for validation. Since a materiality process is not an objective analysis but rather a judgement from various perspectives, results are adjusted if necessary. The final decision on your company’s priorities ultimately lies with the management.

What distinguishes our approach?

We follow a three-dimensional approach that links strategy and reporting and ensures connectivity to key reporting standards (e.g., GRI, International Integrated Reporting Council [IIRC]) and regulatory requirements (e.g., European Non-financial Reporting Directive [EU Directive 2014/95/EU]).

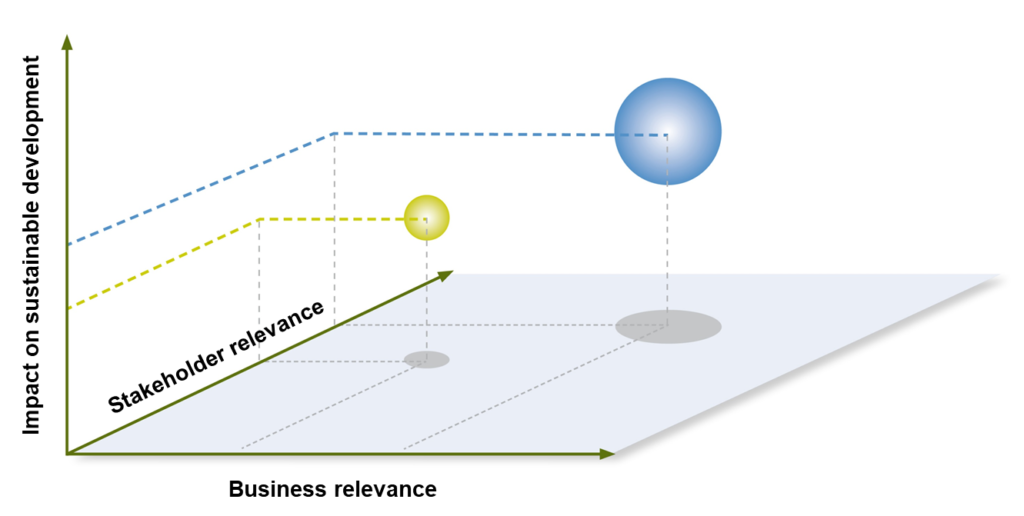

Three dimensions of materiality

Business relevance

The business relevance is usually assessed by management representatives to prioritize topics that are central to long-term business success.

- This perspective is relevant for reporting in accordance with the European Non-Financial Reporting Directive and the recommendations of the IIRC.

Stakeholder relevance

To determine stakeholder relevance, the expectations and needs of the company’s most important stakeholders are assessed and prioritized.

- This perspective is relevant for reporting in accordance with the European Non-Financial Reporting Directive and the GRI Standards (Universal Standards 2016).

Impacts on sustainable development

To assess the impact on sustainable development, the topics where your company has the greatest positive or negative impact on the economy, society, and the environment along its value chains are prioritized.

- This perspective is relevant for reporting in accordance with the GRI standards and the recommendations of the IIRC.

Laying the foundation for your sustainability management

With a systematic materiality assessment that considers various perspectives, you create a solid basis to (further) develop your plan for managing your business sustainably. Strategy, goals and targets, as well as reporting and communication, can thus be aligned along uniform priorities, while strengthening the relationships with your most important stakeholders. To ensure that you do not overlook new business developments and trends, we recommend repeating the assessment at least every two years.